Your results are not only strategy. They are also infrastructure. The same entry and the same stop can behave very differently depending on platform routing, data quality, execution path, and where your setup runs. The goal of this guide is not to “recommend products.” It is to help you build an execution stack that matches your asset class and trading style, then test it before you commit real risk inside prop constraints.

At a glance

- A prop “stack” has three layers: charting front end, execution back end, and monitoring/logging.

- Your stack should be chosen by strategy sensitivity: fills, latency, and data granularity matter more than UI.

- Bridges and copiers add hidden slippage and failure points; they can be fine for swing trading and fatal for micro-scalping.

- VPS is not “to be fast.” It is to be stable, close to the execution server, and online during your trading window.

- Before you size up, run a short stack test: spreads, slippage, rejects, disconnects, and end-to-end latency.

The 3-layer stack model

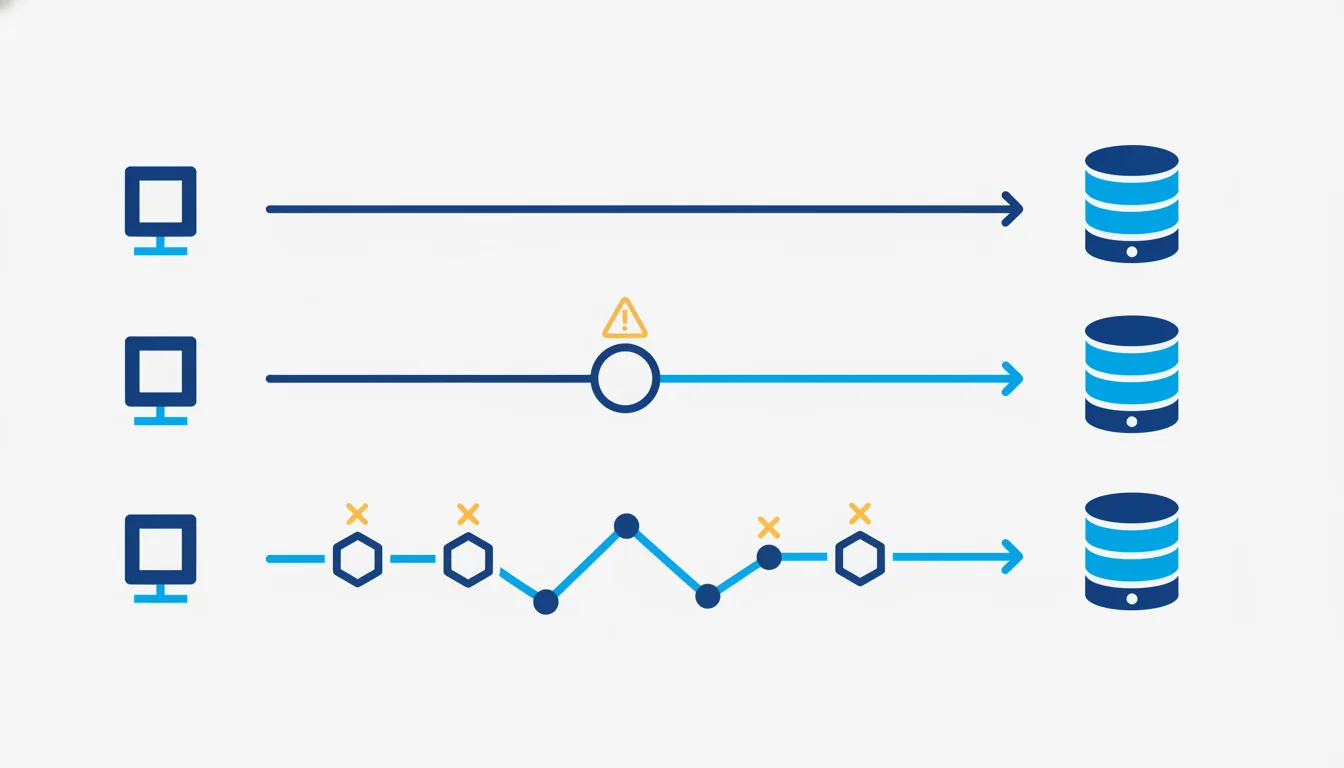

Think in layers. Most traders accidentally build stacks backwards (pretty charting first, then hope execution behaves). Build forward from the execution path.

- Layer 1: Charting front end (where decisions are made). Examples: platform charts, external charting, DOM/footprint UI.

- Layer 2: Execution back end (where orders actually route). This includes the trading server, any bridge, and any risk plugins.

- Layer 3: Monitoring + logging (how you catch problems early). Logs, trade journal fields, alerts, and a “kill switch” process.

When traders say “the market changed,” it is often Layer 2 changing: different fill engine, different routing, different risk plugin behavior, or different liquidity conditions at the time you trade. Your stack should make those changes visible and measurable.

Bridges, copiers, and alert pipelines are not “bad.” They are extra hops. Extra hops mean more points where delays, rejects, or silent failures can appear. If your strategy can tolerate that (swing/intraday with wider stops), you can use them safely. If your strategy depends on tight stops and fast entry, simplify Layer 2 as much as possible.

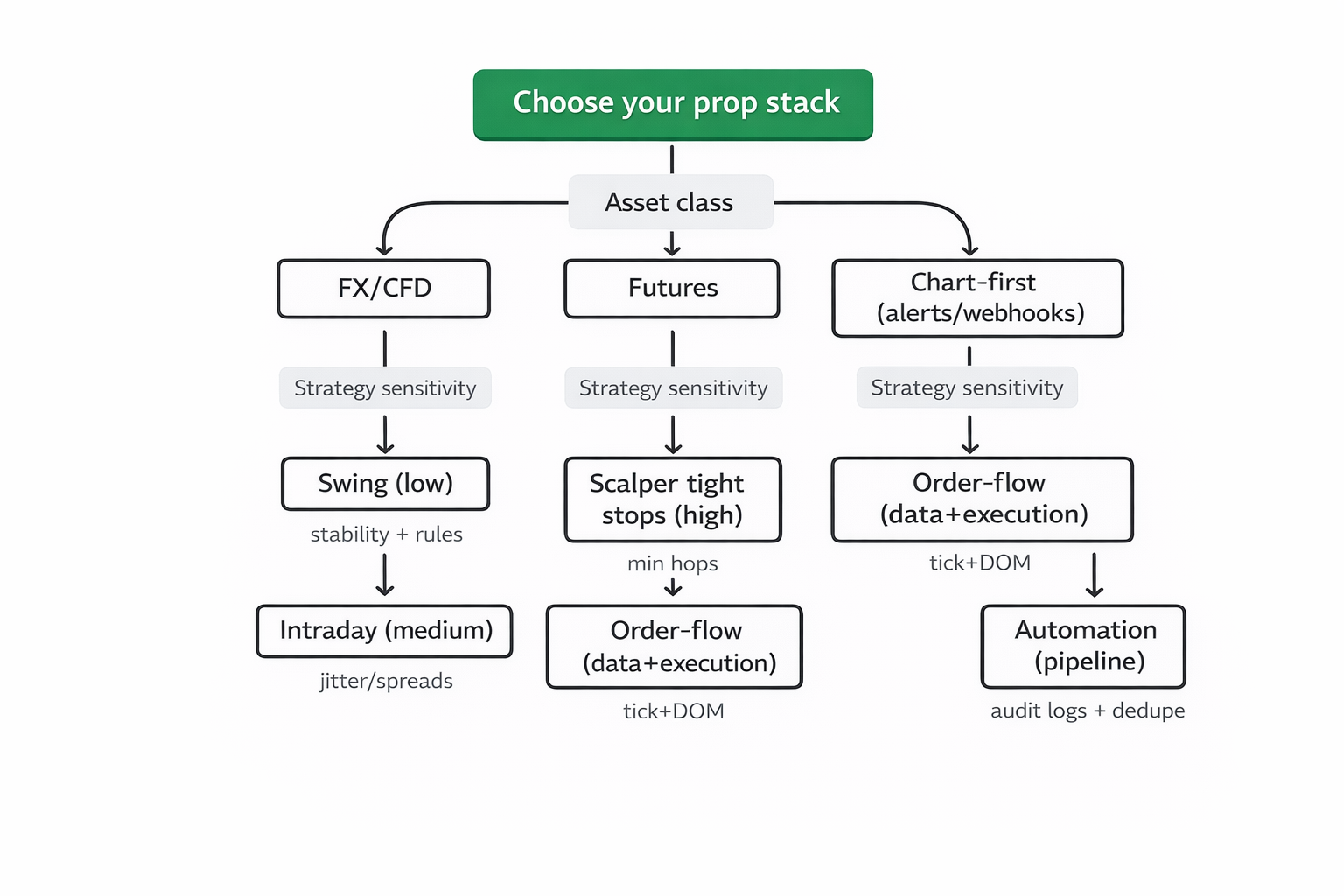

Decision tree: choose by asset class first

Start here. Your asset class determines the minimum viable data + execution choices.

A) FX/CFD (often MT5-based in prop environments)

For FX/CFD props, the common reality is: platform choice is constrained, and execution quality depends heavily on the firm’s liquidity + bridging setup. Your stack is about reducing friction, measuring spreads/slippage, and preventing rule breaches from spikes.

B) Futures (often routed via a futures data/execution stack)

For futures, the critical differentiators are data granularity (tick + depth) and consistency of execution acknowledgements under load. If you trade order-flow, your stack is a data and DOM problem as much as a strategy problem.

C) “Chart-first” workflows (TradingView signals, webhook routing, automation middleware)

Chart-first execution can be clean for swing and structured intraday. It becomes fragile when your edge depends on fast entry or tight stops. If you route alerts into another execution environment, your Layer 2 becomes a pipeline with delays, retries, and failure modes you must plan for.

Decision tree: choose by strategy sensitivity

Now choose your “stack archetype” by how sensitive your strategy is to execution friction.

1) Discretionary swing trader (low sensitivity)

Swing strategies usually survive moderate latency and imperfect fills because the target is large relative to spread and slippage. Your priorities are stability, risk rule awareness, and clean monitoring.

Recommended stack archetype

- Charting front end: Whatever keeps you consistent (platform charts or external charting).

- Execution back end: Direct platform execution (avoid unnecessary bridges if you can).

- Monitoring/logging: Daily loss proximity tracker, spread snapshots at entry time, simple outage plan (mobile backup, flatten protocol).

What to test before committing: average spread during your entries, worst spread you see during your trade window, and whether stops/limits behave as expected during a fast move.

2) Intraday discretionary trader (medium sensitivity)

Intraday edges often depend on clean entries around session opens, breakouts, or mean reversion turns. Moderate latency is fine. Jitter and spread expansion are the real tax.

Recommended stack archetype

- Charting front end: Fast execution UI + stable hotkeys/order panel.

- Execution back end: As direct as possible; minimize alert-to-execution hops.

- Monitoring/logging: End-to-end timing log (signal time → order send → order ack), reject/error code log, and a daily “risk stop” tighter than firm maximum.

What to test before committing: fill quality during your exact session window (not midday), and how your platform behaves during news or fast candles (freezes, disconnects, delayed acks).

3) Scalper / breakout trader with tight stops (high sensitivity)

If your typical stop is small, your stack matters as much as your setup. Spread + commission + slippage can flip expectancy. Bridges and copiers can quietly destroy a scalper’s edge.

Recommended stack archetype

- Charting front end: Execution-first UI (fast order entry, OCO support if relevant, reliable DOM if you use it).

- Execution back end: Avoid multi-hop routing. Prefer the simplest path from your order to the server that enforces risk.

- Monitoring/logging: Slippage distribution log (normal vs fast markets), jitter log, and a “trade no-trade” filter for wide spread/low liquidity windows.

What to test before committing: (1) slippage clustering (how bad it gets during fast moments), (2) partial fill frequency (if applicable), and (3) whether your stop behavior matches your mental model.

4) Order-flow futures trader (data sensitivity + execution sensitivity)

Order-flow depends on granular data. If your feed is delayed, filtered, or thin, you are reading a distorted market. Your stack must prioritize tick accuracy, depth stability, and DOM responsiveness under load.

Recommended stack archetype

- Charting front end: DOM/footprint capable interface with stable performance.

- Execution back end: Futures-appropriate routing with reliable acknowledgements (watch for throttling/order-rate limits).

- Monitoring/logging: Message-rate awareness, rejected order reasons, and a hard daily stop that triggers a flat + lockout routine.

What to test before committing: data stability during peak volume, DOM “stutters,” and how quickly you can flatten during a volatility spike without platform lag.

5) TradingView alert automation (pipeline sensitivity)

Alert-driven systems are operational systems. Your edge depends on the reliability of a pipeline: alert generation, webhook delivery, middleware logic, and execution confirmation. Your biggest risk is not only latency. It is silent failures and duplicated orders.

Recommended stack archetype

- Charting front end: TradingView charts + alert rules designed for stability (avoid overfitting to micro-moves).

- Execution back end: Middleware that can confirm receipt, prevent duplicates, and fail safely (do nothing on uncertainty).

- Monitoring/logging: Alert audit log (alert ID, timestamp, payload), execution acknowledgment log, and an outage mode (pause automation automatically).

What to test before committing: dropped alerts, delayed alerts, duplicate alerts, and mismatch between intended size and executed size.

The “stack test” before you commit size

Run a short test before you treat the stack as trustworthy. The goal is to measure friction and failure modes, not to make money.

- Spread audit: capture spread at entry time for 30–50 trades; note worst spread you see.

- Slippage audit: log expected price vs average fill vs exit; separate normal vs fast conditions.

- Reject audit: log all rejected orders and their reasons; fix systematic causes (order type, size, rate limits).

- Disconnect audit: document any freezes/disconnects and what you did; build a flatten protocol.

- End-to-end timing: signal time → order send → order acknowledged. Watch variability (jitter) more than averages.

If you want one extra safeguard, add a “go/no-go” rule to the test: if spreads exceed your threshold, if rejects appear for non-obvious reasons, or if acknowledgment time becomes unstable, you reduce size or stand down until the stack behaves predictably again.

A simple rule: build for your worst day

Your stack is “good” if it behaves predictably on volatile days, not if it feels fast on calm days. Choose simplicity for sensitive strategies, measure execution drag early, and only scale after you have stable metrics inside your actual prop environment.

If you trade inside prop drawdown constraints, pair this with a clear rule-math model and a daily risk stop that is tighter than the firm maximum.