Instant Funding Forex Prop Firms in 2026

Skip the evaluation and start trading funded capital from day one. We explain how instant funding works, what it costs, who it’s actually built for, and how the top firms compare on price, drawdown, and payout speed.

TL;DR Summary

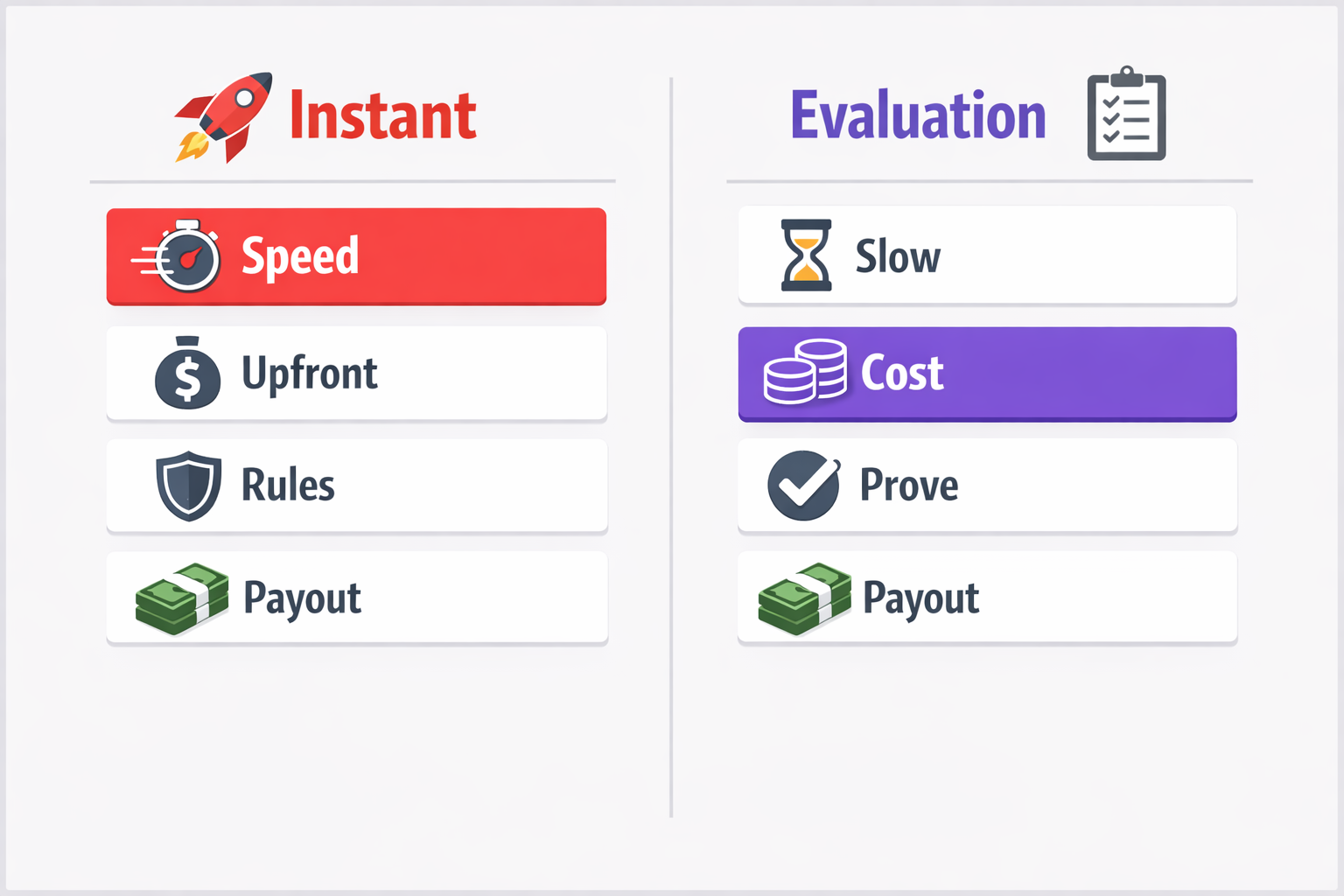

- Instant funding = pay a fee, skip the challenge, receive a funded account within hours. No evaluation phase, no profit targets to pass first.

- Cheapest: MyFundedFX ($399 for 50K) – but tightest drawdown at 5%

- Best Balance: E8 Funding ($488, 8% drawdown, 80% split) or The5ers ($475, immediate payouts)

- Best For: Experienced intraday traders with a proven track record who value time over fee savings

- Skip If: You’re still developing your strategy or haven’t proven consistent profitability. The evaluation route is cheaper and more forgiving.

- Not Available: FTMO (evaluation only, no instant funding path)

What Is Instant Funding?

Not everyone wants to spend weeks proving themselves in an evaluation. Some traders already know they can perform – they’ve been profitable in personal accounts for years, they’ve passed challenges at other firms, or they simply don’t have the patience to grind through a two-phase process before touching funded capital. For those traders, instant funding exists.

The concept is exactly what it sounds like: you pay a fee, skip the evaluation entirely, and receive a funded account ready to trade. No profit targets to hit first. No minimum trading days to clock. You’re live from day one. It’s the fastest path to trading with someone else’s money – but speed comes with trade-offs that are worth understanding before you hand over your card details.

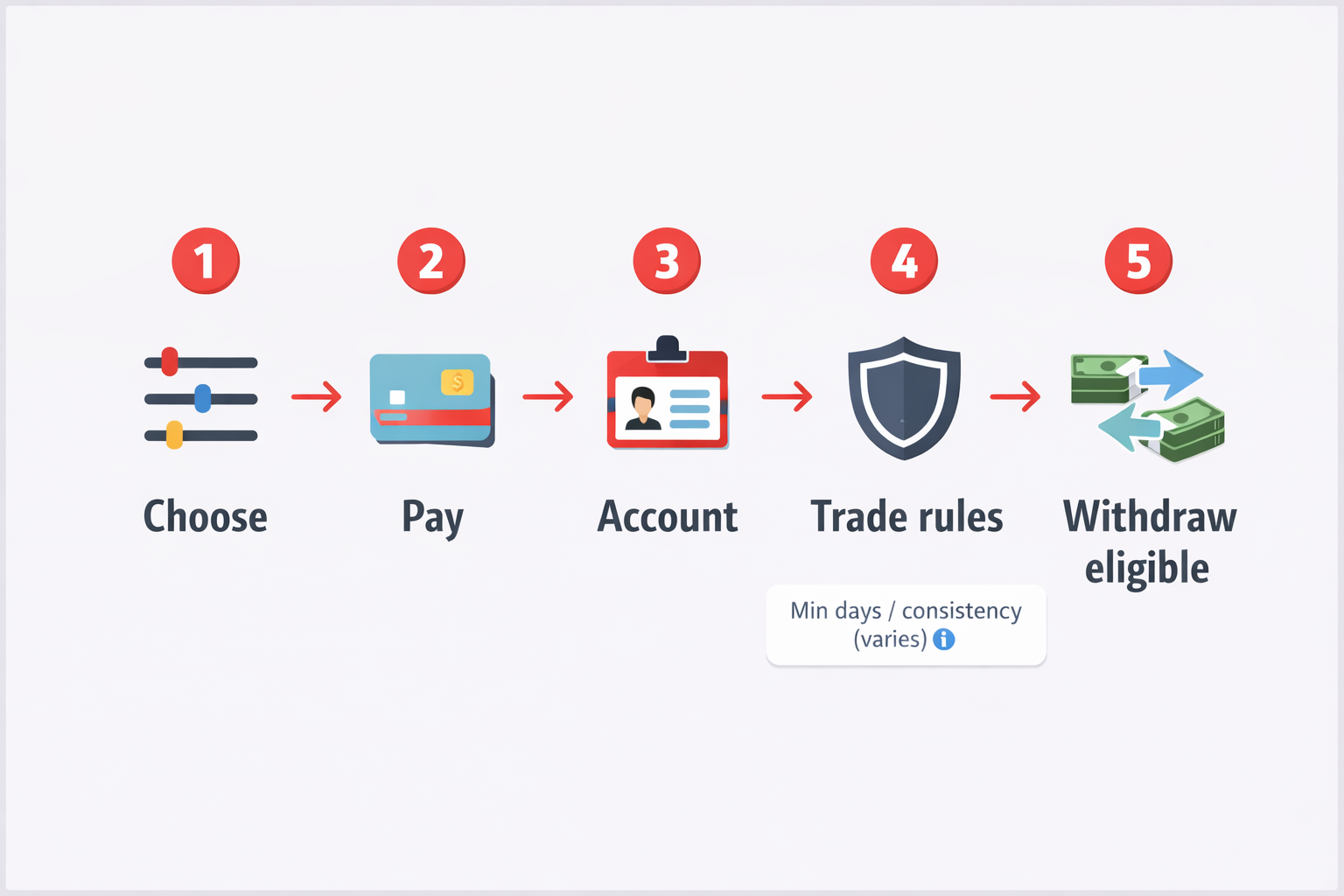

How Instant Funding Actually Works

The process is deliberately simple. You choose an account size, pay the corresponding fee, and the firm provisions your funded account – usually within a few hours, sometimes within minutes. There’s no challenge phase, no verification step, no demo period. You’re trading on the firm’s capital immediately.

That said, “no evaluation” doesn’t mean “no rules.” Instant funded accounts still come with risk parameters. You’ll have a maximum drawdown limit, usually both daily and overall. Some firms add consistency requirements or minimum trading day thresholds before your first withdrawal becomes available. The challenge is removed, but the guardrails stay in place – the firm is still handing you real capital and needs to manage its exposure.

“Instant funding removes the audition, not the expectations. Traders who treat it as a shortcut to reckless risk-taking are the ones who blow the account in the first week.” – Marcus Webb, risk management director at a London-based prop firm

Instant Funding vs. Traditional Evaluations

The difference goes beyond just skipping a test. The entire cost structure, risk profile, and trader experience shifts depending on which model you choose. Here’s where they diverge:

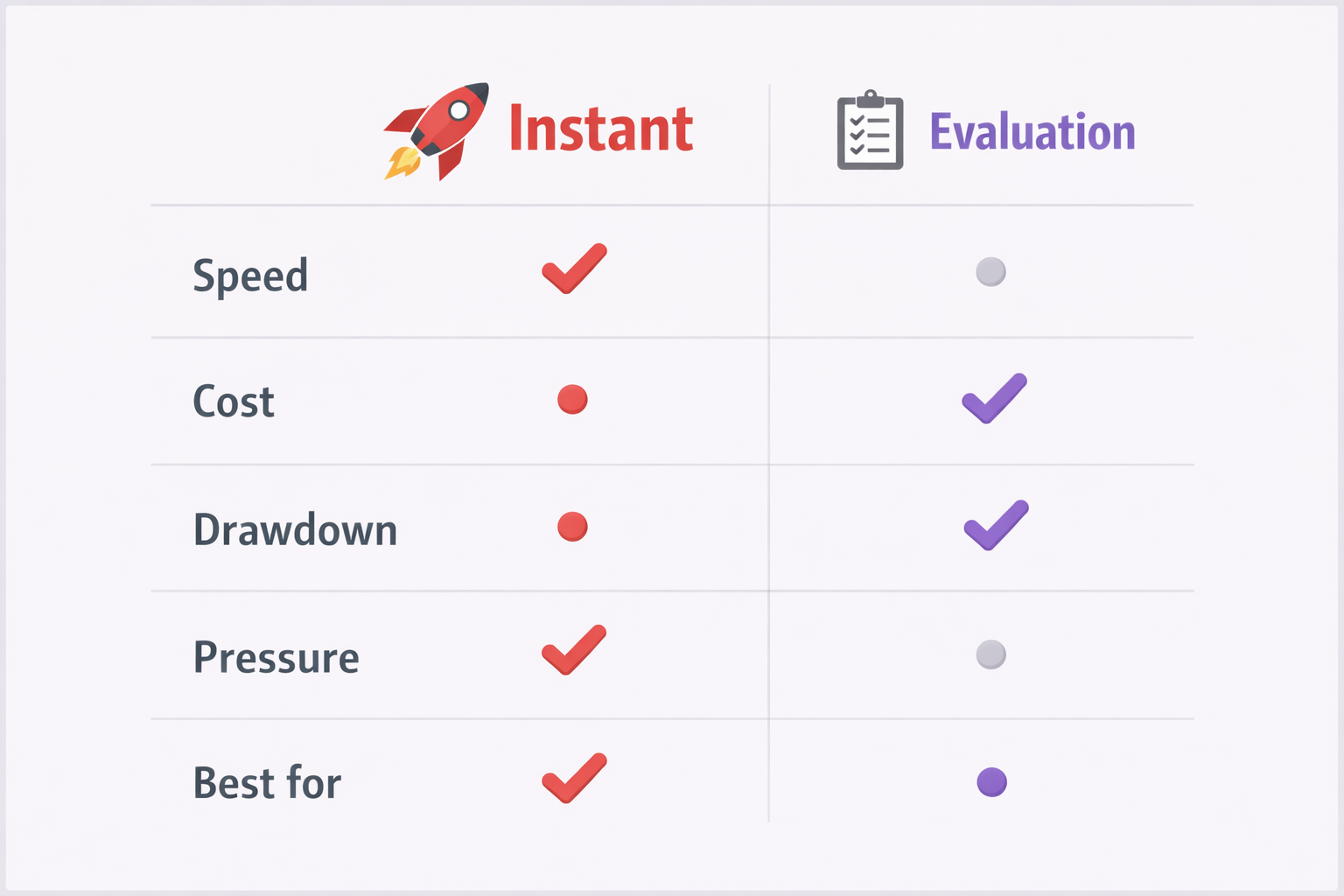

- • Cost. Instant funding accounts are more expensive upfront – often 2x to 3x the price of an equivalent evaluation. A $50K challenge might cost $200–$300, while an instant funded account at the same size typically runs $350–$600. You’re paying a premium for immediate access.

- • Profit split. Some firms offer the same profit split across both models, but others reduce the split on instant accounts. Where a standard evaluation might get you 80–90%, the instant equivalent could sit at 60–80%.

- • Drawdown rules. Instant funded accounts often come with tighter drawdown limits than post-evaluation accounts. A firm might give you a 10% max drawdown after passing a challenge but only 6–8% on an instant account.

- • Time to first payout. With evaluations, you might spend 2–8 weeks passing before you can even start earning. Instant funding lets you book profits from day one, meaning your time-to-payout is dramatically shorter – assuming you’re profitable immediately.

Neither model is objectively superior. It depends entirely on where you are as a trader. Someone who’s consistently profitable and values their time over the extra cost will lean toward instant funding. A trader who’s still building confidence or wants to minimize upfront spend is usually better served by the evaluation route.

Top Instant Funding Firms – Reviewed

All pricing based on the $50K instant funding tier. Each review covers the fee, drawdown, profit split, and what makes the firm worth considering – or not.

MyFundedFX – Lowest Price Point

The cheapest instant funding option among established firms. MyFundedFX offers $50K instant accounts for $399 with an 80% profit split and a 5% maximum drawdown. First payout is available after 5 trading days, processed bi-weekly. The price is unbeatable, but that 5% drawdown is the tightest on this list – giving you exactly $2,500 of breathing room on a $50K account.

The5ers – Fastest Payout Access

The5ers charges $475 for a $50K instant account with an 80% profit split and 6% drawdown. The standout feature: immediate payout eligibility with on-demand withdrawals. No waiting period, no minimum trading days before your first withdrawal.

E8 Funding – Best Drawdown Buffer

E8’s instant account is priced at $488 with an 80% profit split and the most generous drawdown on this list: 8% maximum. That’s $4,000 of breathing room on a $50K account. First payout available after 7 trading days, processed bi-weekly.

Funded Next – Best Scaling Potential

Funded Next prices their $50K instant account at $549. The initial profit split starts at 60%, scaling to 90% based on consistent performance. Drawdown is 6% static, and the first payout requires 5 trading days of activity.

SurgeTrader – On-Demand Payouts

SurgeTrader offers instant funding at $525 with a 75–90% profit split (scaling) and 5% drawdown. Their payout model is on-demand after the first trade cycle.

FundingPips – No Account Limits

FundingPips offers instant funding with no cap on the number of accounts a trader can hold. Their $50K instant account is ~ $499 with an 80–90% profit split (scaling) and 6% static drawdown. Payouts are processed within 24 hours.

Blueberry Funded – Broker-Grade Execution

Backed by Blueberry Markets. Priced at ~ $499 for $50K with an 80% profit split and 6% drawdown. The edge is execution quality (tighter raw spreads and faster fills).

NOT AVAILABLE: FTMO

FTMO does not offer an instant funding path as of writing. All traders must complete their 2-step evaluation process before receiving funded capital.

Full Comparison Table

All figures based on $50K instant funding tier. FTMO included for reference (evaluation only).

Sorted by price, low to high. MyFundedFX is the cheapest but has the tightest drawdown. E8 Funding’s 8% buffer gives the most room to trade naturally. The5ers is the only firm offering immediate payouts with no waiting period. Funded Next is the most expensive upfront but offers the highest ceiling at 90% split – though you start at 60%. SurgeTrader’s trailing drawdown at 5% makes it the riskiest proposition for active daily traders.

“Instant funding is the litmus test for how much a trader trusts their own edge. If you’re not willing to bet $400–$500 that you’ll be profitable from day one, the evaluation is probably the smarter path.” – Alicia Torres, proprietary trading strategist

Who Should Actually Consider Instant Funding

Instant funding isn’t for beginners. That’s arithmetic. The higher upfront cost, tighter drawdowns, and immediate live conditions mean the margin for learning on the job is razor-thin. If you’re still developing your strategy or haven’t proven consistent profitability on a personal account, an evaluation-based firm gives you a cheaper, lower-pressure entry point.

Instant funding makes the most sense for:

- • Experienced traders with a proven track record who want to skip the evaluation process they’ve already completed elsewhere.

- • Full-time traders who value time as a cost.

- • Strategy-specific traders (news, high-volatility breakouts, etc.) that don’t fit evaluation constraints cleanly.

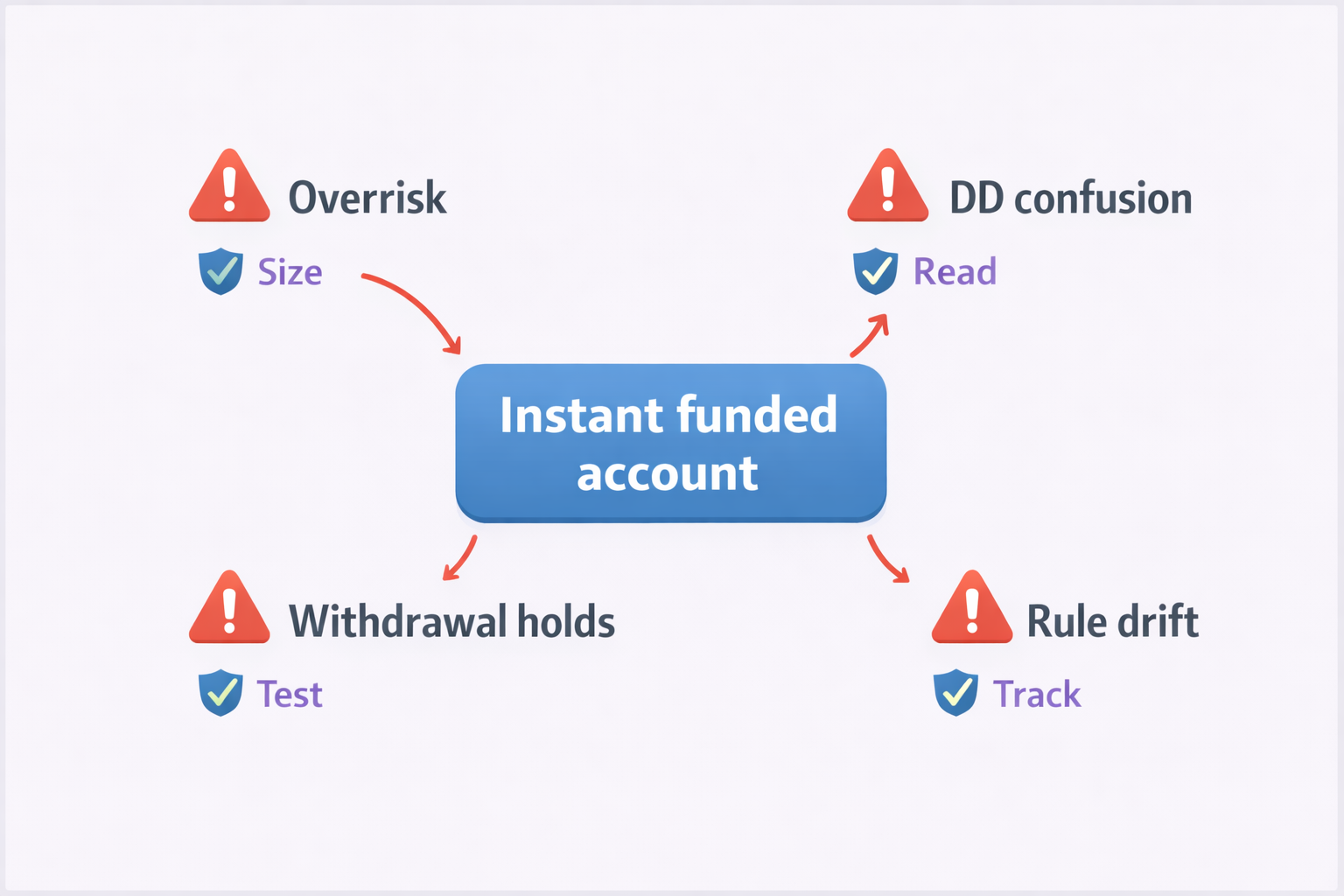

What Can Go Wrong

Instant funding’s biggest risk is the one nobody markets: overconfidence. Skipping the evaluation creates a psychological shortcut where traders assume readiness without testing it. An evaluation, for all its frustrations, forces you to prove consistency under defined conditions. Without that filter, the only thing standing between a new instant account and a blown one is your own discipline.

There’s also a sunk cost trap. With a $200 evaluation, failing feels manageable. With a $500 instant account, the pressure to “make it work” can lead to revenge trading, oversizing positions, or abandoning your plan when the first few trades go sideways.

“The traders who succeed with instant funding are the ones who would have passed the evaluation anyway.” – David Linh, head of trader development at a Singapore prop desk

Pros and Cons of Instant Funding

Tips for Getting the Most Out of Instant Funding

- Start smaller than you think you need. Get comfortable with the firm’s platform, spreads, and execution before sizing up.

- Know your drawdown to the decimal. Make sure your historical variance fits inside the buffer.

- Withdraw early and often. Lock in gains and reduce emotional attachment to the balance.

- Compare the instant fee to your evaluation failure rate. Be honest about your pass rate and total spend.

- Read scaling terms. If you plan to stay long-term, scaling matters more than entry price.

Final Thought

Instant funding is growing fast, and competition among firms is driving both prices down and terms up. The firms that will win long-term are the ones that combine fair pricing with genuine drawdown flexibility and reliable payouts – not the ones racing to the cheapest fee with razor-thin margins of error.

Frequently Asked Questions

Is instant funding real capital or a simulated account?

This varies by firm. Some accounts trade on live liquidity; others use simulated environments. In both cases, the profits you withdraw are real money. If execution mechanics matter to your strategy, confirm the firm’s setup before purchasing.

Can I get a refund on an instant funded account?

Generally no. Instant funding fees are typically non-refundable. Some firms may offer credit toward a new account, but outright refunds are rare.

Why doesn’t every firm offer instant funding?

Risk management. Evaluations filter out unprofitable traders before capital allocation. Instant funding shifts risk forward, which firms offset via higher fees, tighter drawdowns, or lower splits.

How do I know if I’m ready for instant funding?

If you’re consistently profitable with a stable drawdown (often within ~4–6% over recent months), you’re closer to ready. If your results rely on outsized wins or include sharp equity drops, evaluation is usually a safer, cheaper stress test.

Which instant funding firm has the best drawdown buffer?

E8 Funding, with an 8% maximum drawdown on their instant accounts.

Disclaimer

The information provided on this page is for educational and informational purposes only. It does not constitute financial advice, trading recommendations, or endorsement of any specific prop firm. Instant funding fees, drawdown limits, profit splits, and payout terms are subject to change without notice. Always verify current terms directly with the firm before committing capital. Trading involves significant risk of loss.